Education Loan for MS in USA Without Collateral 2026: A Complete Guide for Indian Students

edubeatsworld.com

5/15/2026

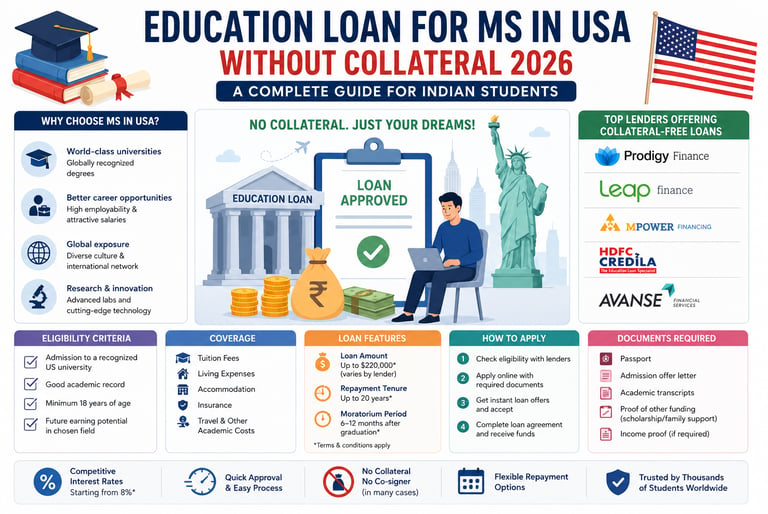

Pursuing a Master’s degree in the United States continues to be one of the biggest academic aspirations for Indian students in 2026. American universities are globally respected for their advanced research facilities, industry exposure, innovation-driven education, and strong career opportunities. Degrees from US universities often open doors to international careers, higher salaries, and global networking opportunities.

However, while the dream is attractive, the financial investment can feel overwhelming for many families. Tuition fees for MS programs in the US can range from ₹20 lakhs to ₹60 lakhs or more depending on the university and course. Along with tuition, students also need to consider living expenses, accommodation, insurance, books, transportation, visa charges, and travel costs.

In the past, many students struggled because banks demanded collateral such as property, fixed deposits, or other valuable assets before sanctioning large education loans. Today, the situation has changed significantly. Several Indian and international lenders now provide education loans for MS in the USA without collateral, especially for students admitted to reputed universities and career-oriented programs.

These collateral-free loans have made overseas education more accessible for deserving students who may not have strong financial assets but possess good academic potential and promising career prospects.

This detailed guide explains everything students should know about collateral-free education loans for MS in the USA in 2026 — including lenders, eligibility, repayment options, required documents, approval tips, and important precautions before taking a loan.

(“Many students planning higher education abroad also explore affordable destinations and visa preparation strategies.”)

Understanding Collateral-Free Education Loans

A collateral-free education loan is a study loan that does not require students or parents to pledge any security or property against the borrowed amount. Traditional education loans from many banks usually require collateral for high-value overseas education loans. This may include:

Residential property

Commercial property

Fixed deposits

Insurance policies

Non-agricultural land

For many middle-class families, arranging such collateral becomes difficult or risky. Collateral-free loans solve this issue by assessing the student’s future earning capacity instead of relying completely on family assets.

Modern lenders now focus on:

Academic performance

Reputation of the university

Employability after graduation

Course demand in the job market

Expected future salary

This approach has expanded educational opportunities for thousands of Indian students planning to study abroad.

Why Demand for No-Collateral Loans Is Increasing in 2026

The popularity of collateral-free education loans has increased rapidly in recent years. One major reason is the growing awareness among students about international education opportunities. Another reason is the rise of fintech companies and international lenders that provide simplified digital loan processes.

Students today prefer no-collateral loans for several practical reasons.

Reduced Financial Risk for Families

Many parents hesitate to mortgage their home or property because repayment uncertainty can create emotional and financial pressure. A collateral-free loan removes this burden and gives families more confidence to support overseas education plans.

Faster Approval Process

Traditional secured loans may involve:

Property verification

Legal checks

Valuation reports

Physical bank visits

This process can take several weeks. In contrast, many modern lenders provide online approvals within days after document submission.

Easier Access for Middle-Class Students

Students from academically strong backgrounds may now receive funding even if their families do not own large assets. This has widened opportunities for talented students from diverse economic backgrounds.

Flexible Repayment Options

Many lenders now offer flexible repayment structures where students begin repayment only after completing their course and securing employment.

Cost of Pursuing an MS in the USA in 2026

Before applying for a loan, students should understand the approximate total cost of studying in the USA.

Tuition Fees

Tuition fees vary according to:

University ranking

Course specialization

Public or private university

Duration of the program

On average:

Public universities may charge ₹18–35 lakhs

Private universities may charge ₹35–60 lakhs or more

Courses such as Data Science, Artificial Intelligence, Computer Science, and MBA-related programs are often more expensive.

Living Expenses

Living costs depend heavily on the city and lifestyle. Students studying in cities like:

New York

Boston

San Francisco

Los Angeles

may spend significantly more compared to smaller towns.

Average yearly living expenses may include:

Accommodation

Food

Transportation

Utilities

Internet

Personal expenses

These may collectively range from ₹8–18 lakhs annually.

Additional Expenses

Students should also budget for:

Visa application fees

Flight tickets

Health insurance

Laptop and study materials

Emergency funds

A realistic financial plan helps avoid future stress and borrowing complications.

Best Lenders Offering Education Loans Without Collateral

Several lenders in India and abroad now specialize in student financing for international education.

1. Prodigy Finance

Prodigy Finance Official Website

Prodigy Finance is among the most recognized international education financing companies for postgraduate students. It primarily supports students pursuing master’s programs at globally reputed universities.

What Makes Prodigy Finance Popular?

Unlike traditional banks, Prodigy Finance evaluates:

University ranking

Future earning potential

Course demand

Career opportunities after graduation

rather than depending mainly on family income or collateral.

Loan Coverage

The loan may cover:

Tuition fees

Living expenses

Insurance

Other academic costs

In many cases, students can receive funding close to the total cost of attendance.

Repayment Structure

Repayment generally begins after course completion and grace period. Loan tenures may extend up to 20 years depending on the loan amount and profile.

Important Consideration

Since many international lenders provide variable interest rates, students should understand how global market fluctuations may affect repayment amounts in the future.

2. Leap Finance

Leap Finance has become highly popular among Indian students because of its student-friendly application process and fast loan sanctions.

Key Advantages

Leap Finance offers:

Quick online applications

Minimal paperwork

Flexible repayment terms

No collateral for eligible profiles

Focus on Indian Students

The platform specifically understands the challenges faced by Indian students applying abroad. Many applicants appreciate its digital-first approach and faster communication process.

Loan Approval Factors

Approval usually depends on:

University reputation

Academic background

Course employability

Expected future income

Strong STEM programs often receive better approval chances.

3. MPOWER Financing

MPOWER Financing Official Website

MPOWER Financing mainly focuses on international students studying in the US and Canada.

Why Students Consider MPOWER

One of the biggest benefits is that students may not require:

Collateral

Co-signer

US credit history

This becomes especially helpful for students whose parents may not have strong financial documentation.

Additional Student Support

Apart from loans, MPOWER also offers:

Career guidance

Scholarship opportunities

Visa support resources

Internship preparation support

This makes it more than just a financing platform.

4. Avanse Financial Services

Avanse provides customized education financing solutions for students studying abroad.

Loan Features

Depending on the student profile and university, Avanse may provide:

Partial unsecured loans

Flexible moratorium periods

Extended repayment tenures

Important Note

For very high loan amounts, partial collateral may sometimes still be requested depending on risk assessment.

5. HDFC Credila

HDFC Credila remains one of India’s leading education loan providers for overseas studies.

Why Many Students Choose Credila

Students often consider Credila because of:

Large loan amounts

Broad university coverage

Structured repayment options

Experience in overseas education financing

Loan Flexibility

The lender may offer both secured and partially unsecured loan structures depending on:

Student profile

Course

Co-applicant income

University ranking

Eligibility Criteria for Collateral-Free Loans

Different lenders have different approval policies, but certain common factors are considered almost everywhere.

Strong Academic Performance

Good academic records improve approval chances because lenders view such students as lower-risk borrowers.

Students with:

Higher CGPA

Strong GRE or GMAT scores

Good English proficiency scores

often receive better loan terms.

Admission to Recognized Universities

Universities with strong global rankings and employment records improve lender confidence. Courses from reputed institutions are considered safer investments because graduates usually have better job prospects.

Employability of the Course

Lenders carefully analyze whether the chosen field has good employment opportunities.

Programs commonly preferred include:

Computer Science

Artificial Intelligence

Data Analytics

Cybersecurity

Engineering

Finance

Healthcare Technology

These fields are considered high-growth sectors.

Co-Applicant Profile

Some lenders may still evaluate parental income even if collateral is not required. Stable financial background strengthens the application.

Documents Required for the Loan Process

Students should organize all documents early to avoid delays.

Personal Identification Documents

Typically required documents include:

Passport

Aadhaar card

PAN card

Passport-sized photographs

Academic Documents

Students must usually submit:

Academic transcripts

Degree certificates

Entrance exam scores

University admission letter

These documents help lenders evaluate academic potential.

Financial Documents

Depending on the lender, students may also need:

Parent income proof

Salary slips

Income tax returns

Bank statements

Additional Supporting Documents

Some lenders may ask for:

Resume or CV

Statement of Purpose

Scholarship proof

Internship experience documents

These can strengthen the overall profile.

Expenses Covered Under the Loan

Many students mistakenly believe that education loans only cover tuition fees. In reality, most international education loans may include multiple academic and living expenses.

These often include:

Tuition fees

Hostel or rent expenses

Food and daily living expenses

Health insurance

Air travel

Visa charges

Books and equipment

Laptop purchase

Examination fees

Students should confirm exact coverage details before accepting the loan agreement.

(Strong IELTS scores and academic performance can strengthen university applications.”)

Understanding Interest Rates

Interest rates are one of the most important aspects of any education loan.

Fixed Interest Rate

A fixed rate remains constant throughout the loan tenure. This provides predictable EMI payments.

Floating or Variable Interest Rate

Variable interest rates may increase or decrease according to market conditions. While initial rates may appear lower, repayment amounts can change over time.

Students should calculate long-term repayment costs before finalizing the loan.

Repayment Structure Explained

Understanding repayment conditions is essential before borrowing large amounts.

Moratorium Period

Most lenders provide a moratorium period which includes:

Course duration

Plus 6–12 months after graduation

This allows students time to secure employment before starting full repayment.

Simple Interest During Study

Some lenders ask students to pay only simple interest while studying. Doing this can significantly reduce future EMI burden.

EMI Repayment After Graduation

Once the grace period ends, regular monthly repayment begins.

Students should estimate:

Expected salary

Living costs abroad

Currency conversion impact

before choosing loan tenure.

Tips to Improve Approval Chances

Apply Early

Applying early gives students more time to compare lenders and complete documentation.

Select Career-Oriented Courses

Courses with strong employment demand improve lender confidence.

Maintain Transparency

Students should provide accurate information in applications. Incorrect financial details may lead to rejection.

Compare Multiple Loan Offers

Students should compare:

Interest rates

Processing fees

Repayment flexibility

Currency terms

Penalties

before making a decision.

Common Mistakes Students Should Avoid

Many students focus only on getting quick approval and ignore long-term repayment consequences.

Avoid these mistakes:

Ignoring processing fees

Not checking currency risks

Borrowing more than required

Not understanding variable interest rates

Ignoring repayment penalties

Failing to compare lenders

Careful planning can prevent future financial pressure.

Is Taking a No-Collateral Education Loan Worth It?

For many students, the answer depends on:

Career goals

University quality

Expected salary after graduation

Financial discipline

An MS degree from a reputed US university can create strong professional opportunities. However, students should choose courses wisely and calculate realistic repayment capacity before borrowing large amounts.

A loan should be viewed as an investment in education rather than immediate financial burden — but only when planned responsibly.

Frequently Asked Questions (FAQs)

Can I get an education loan for MS in the USA without collateral in 2026?

Yes. Many Indian and international lenders now offer collateral-free education loans for students pursuing MS programs in the USA. Approval usually depends on factors such as academic performance, university ranking, employability of the course, and future earning potential rather than property or assets.

Which lenders provide no-collateral education loans for Indian students?

Some of the popular lenders include:

· Prodigy Finance

· Leap Finance

· MPOWER Financing

· HDFC Credila

· Avanse Financial Services

Each lender has different eligibility requirements, repayment structures, and interest rates.

What is the maximum loan amount students can receive?

The loan amount varies depending on:

· University

· Course

· Student profile

· Expected future salary

· Cost of attendance

Some lenders may provide funding close to 100% of the total education cost, including tuition and living expenses.

Do students need a co-applicant for collateral-free loans?

Not always.

Certain international lenders such as Prodigy Finance and MPOWER Financing may offer loans without requiring a co-signer or collateral for eligible universities and programs.

However, many Indian lenders still prefer a parent or guardian as co-applicant.

Are living expenses covered under the education loan?

In many cases, yes.

Most education loans for studying abroad may cover:

· Tuition fees

· Accommodation

· Food expenses

· Health insurance

· Visa fees

· Flight tickets

· Books and laptops

· Other academic expenses

Students should confirm the exact coverage details with the lender before signing the agreement.

What interest rates are usually offered?

Interest rates vary according to:

· Lender

· Student profile

· University ranking

· Loan amount

· Market conditions

Rates may generally begin around 8%–12%, though they can change over time.

What is a moratorium period?

A moratorium period is the duration during which students are not required to make full EMI repayments.

It usually includes:

· Course duration

· Plus 6–12 months after graduation

Some lenders may still ask students to pay simple interest during the study period.

Can students repay the loan early?

Yes, many lenders allow partial or full prepayment. However, students should carefully check:

· Prepayment penalties

· Foreclosure charges

· Processing conditions

before finalizing the loan.

Does getting a loan guarantee a US student visa?

No.

An education loan may strengthen the financial profile of a student during visa processing, but it does not guarantee visa approval. Visa decisions depend on multiple factors evaluated by US authorities.

How to Choose the Right Education Loan

Selecting the right education loan is as important as selecting the right university. Students should avoid choosing a lender solely because of faster approval or lower initial interest rates.

Compare Total Repayment Cost

A lower interest rate may sometimes come with:

· Higher processing fees

· Currency conversion costs

· Insurance charges

Students should calculate the total repayment amount over the entire loan tenure.

Understand Currency Risks

Some international lenders disburse loans in US dollars. If the Indian rupee weakens against the dollar in future, repayment costs may increase.

Students should understand how exchange rate fluctuations can affect long-term repayment.

Evaluate Repayment Flexibility

Good lenders usually provide:

· Longer repayment periods

· Flexible EMI options

· Grace periods after graduation

This helps students manage finances comfortably after securing employment.

Check University Eligibility Lists

Some lenders only support selected universities and programs. Students should verify whether their university is included before applying.

Scholarships and Loan Combination Strategy

Many students reduce loan burden by combining:

· Scholarships

· Assistantships

· Part-time work opportunities

· Education loans

This strategy reduces long-term financial pressure and lowers overall repayment burden.

Students should actively search for:

· Merit-based scholarships

· Departmental grants

· Research assistantships

· Teaching assistantships

offered by universities in the US.

Can Part-Time Jobs Help Repayment?

International students in the USA are usually allowed limited on-campus work opportunities according to visa regulations.

Part-time jobs may help students manage:

· Daily expenses

· Food costs

· Transportation

· Personal spending

However, students should not depend entirely on part-time income for tuition repayment because opportunities and earnings can vary.

Importance of Financial Planning Before Taking a Loan

Students should create a realistic financial roadmap before accepting any loan offer.

This should include:

· Estimated total study cost

· Expected post-graduation salary

· Monthly repayment estimate

· Emergency backup funds

· Currency fluctuation considerations

Responsible financial planning helps avoid repayment stress in future.

Mistakes Students Should Avoid While Applying

Borrowing More Than Necessary

Some students borrow maximum amounts without calculating actual needs. Higher borrowing increases long-term interest burden.

Ignoring Hidden Charges

Students should carefully check:

· Processing fees

· Administrative charges

· Insurance costs

· Currency conversion fees

before accepting loan terms.

Waiting Until the Last Moment

Late applications can create:

· Visa delays

· Admission complications

· Financial uncertainty

Applying early improves preparation and negotiation flexibility.

Not Reading the Loan Agreement Properly

Students should carefully review:

· Interest structure

· Repayment schedule

· Default penalties

· Moratorium conditions

before signing any agreement.

Future Scope After MS in the USA

An MS degree from a reputed US university can open opportunities in:

· Technology

· Artificial Intelligence

· Data Science

· Engineering

· Finance

· Healthcare

· Research sectors

Many students pursue Optional Practical Training (OPT) opportunities after graduation to gain international work experience and strengthen repayment capacity.

However, students should remember that career outcomes depend on:

· Skill level

· Job market conditions

· Networking

· Internship experience

· Academic performance

(Apart from education loans, students should also understand visa procedures, entrance preparation, and alternative study abroad destinations.)

Final Thoughts

Education loans without collateral have become a major support system for Indian students aspiring to pursue an MS degree in the USA in 2026. These financing options have reduced dependence on property-backed loans and made international education more accessible to academically deserving students.

With the rise of fintech lenders and international student financing platforms, students today have more choices, faster approvals, and greater flexibility than ever before. Still, borrowing for overseas education is a major financial decision that requires careful planning and responsible management.

Students should compare lenders thoroughly, understand repayment obligations, calculate future financial responsibilities realistically, and stay updated through official sources before making final decisions.

A well-planned education loan can become an investment in long-term career growth, global exposure, and professional success when approached wisely and responsibly.

Disclaimer

This article titled “Education Loan for MS in USA Without Collateral 2026: A Complete Guide for Indian Students” is intended solely for educational and informational purposes. The content has been prepared using publicly available information, official lender resources, education financing updates, study-abroad related guidance, online research, and general financial information available at the time of publication.

Education loan policies, interest rates, repayment terms, eligibility criteria, university requirements, processing fees, moratorium periods, exchange rate conditions, and documentation requirements may change periodically depending on updates issued by banks, financial institutions, fintech lenders, government authorities, universities, or international education financing providers. Readers are strongly advised to verify the latest information directly through the official websites of lenders, banks, universities, and financial advisors before making any educational, financial, or borrowing decisions.

EduBeatsWorld.com is an independent educational blog and is not affiliated, associated, authorized, endorsed by, or officially connected with any US university, embassy, immigration authority, bank, NBFC, fintech lender, consultancy, or government body. This article does not guarantee education loan approval, university admission, visa approval, scholarships, employment opportunities, repayment success, or financial outcomes in the United States or elsewhere.

Related Articles

contact@edubeatsworld.com

© 2024. All rights reserved.